by Daniel Brouse

July 2026

For generations, real estate has been viewed as one of the safest long-term investments. Land cannot be manufactured, buildings can be improved, and population growth has historically supported rising property values. Climate change is altering many of the assumptions that have underpinned real estate markets for decades.

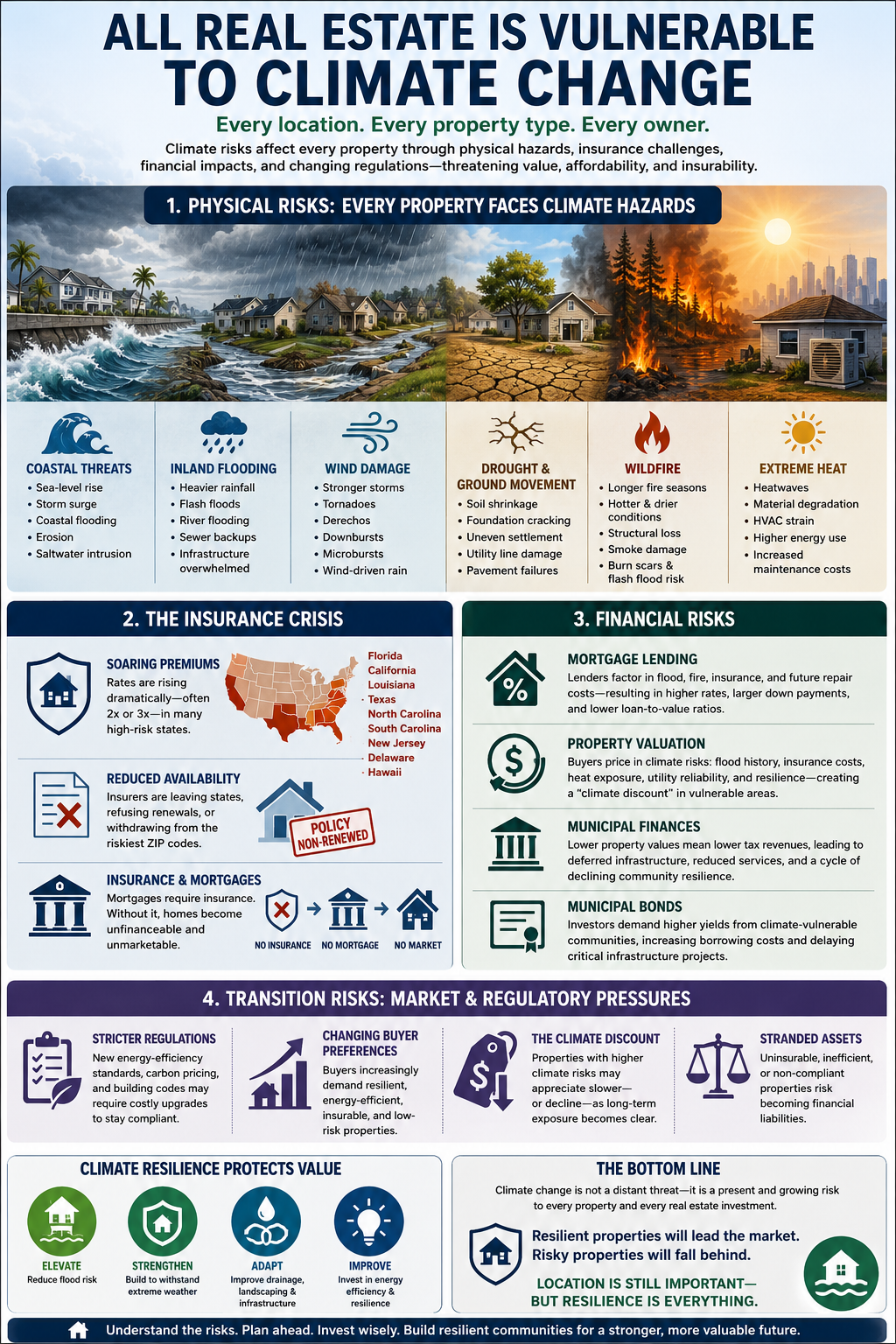

Contrary to popular belief, climate risk is not confined to beachfront homes or wildfire-prone forests. Every property is exposed to climate-related risks, although the specific hazards vary by location. These risks extend far beyond physical damage. They increasingly affect insurance availability, mortgage lending, municipal finances, infrastructure reliability, property values, and long-term market liquidity.

The vulnerability of real estate can be understood through four interconnected categories: physical risks, insurance risks, financial and lending risks, and transition risks.

Extreme Weather Impacts:

Extreme "Energy" Events |

Temperature, Pressure, and Moisture Gradients |

The Reign of Violent Rain |

Floods |

Atmospheric Rivers |

Wildfires |

Microbursts |

Straight-Line Winds

Climate change is increasing both the frequency and intensity of many weather-related hazards. Every region experiences different threats, but no location is completely immune.

Coastal properties face some of the most visible climate risks, including:

Even modest sea-level rise significantly increases flood frequency because storm surges begin from a higher baseline.

Many inland communities once considered “safe” are experiencing increasing flood losses.

Warmer air holds approximately 7% more water vapor for every 1°C of warming, increasing the potential for intense rainfall events. As storms become more moisture-laden, drainage systems designed for twentieth-century rainfall often become overwhelmed.

Consequences include:

Properties located well outside traditional floodplains are increasingly experiencing damaging floods.

For much of the United States, wind represents the largest source of insured property losses.

Climate change is increasing atmospheric energy available for:

Roofs, siding, windows, and mature trees are particularly vulnerable. Wind-driven rain often causes damage even when structures remain standing.

Longer fire seasons, hotter temperatures, and more frequent droughts have dramatically expanded wildfire risk.

Wildfires threaten real estate through:

Burn scars also increase the likelihood of flash flooding and debris flows during subsequent rainstorms.

Extended drought affects soils in complex ways.

Clay-rich soils shrink as they dry, causing:

Conversely, periods of heavy rainfall following drought can produce rapid soil expansion that further stresses structures.

Heat affects virtually every building.

Higher temperatures accelerate deterioration of:

Buildings require more cooling energy while mechanical systems experience greater wear, increasing maintenance and operating costs.

Insurance is becoming one of the most important climate risks facing property owners.

Historically, insurance spread risk across large geographic regions. As climate-related losses increase, that model is becoming increasingly difficult to sustain.

Many homeowners and commercial property owners have experienced substantial premium increases.

States experiencing particularly rapid increases include:

In many communities, insurance costs are rising faster than home values.

Some insurers are:

As private insurers withdraw, many homeowners are forced into state-sponsored insurers of last resort, which often provide less comprehensive coverage at higher cost.

Insurance availability directly affects financing.

Most mortgage lenders require continuous hazard insurance throughout the life of the loan.

If insurance becomes unavailable or unaffordable:

Without insurance, many homes effectively become difficult or impossible to finance.

Climate change affects real estate markets even before disasters occur.

Financial institutions increasingly incorporate climate risk into lending and investment decisions.

Banks and mortgage investors evaluate:

Higher perceived risk may result in:

Properties once viewed as routine collateral may gradually become more difficult to finance.

Real estate markets depend heavily on expectations of future value.

Buyers increasingly consider:

Two otherwise identical homes may command significantly different prices simply because one carries greater long-term climate risk.

Local governments rely heavily on property taxes.

If climate risks reduce property values, municipalities may experience:

This creates a feedback loop in which deteriorating infrastructure further reduces property values.

Cities and counties finance roads, schools, water systems, and flood-control projects through municipal bonds.

Increasing climate risks may lead investors to demand higher yields from municipalities perceived as vulnerable. Higher borrowing costs can delay infrastructure improvements, making communities even more susceptible to future climate impacts.

Credit rating agencies are paying increasing attention to long-term climate resilience when evaluating municipal creditworthiness.

Not all climate risks arise from weather.

Many result from changes in markets, technology, regulations, and consumer preferences.

Governments are gradually adopting stricter standards for:

Older buildings may require expensive upgrades to remain competitive.

Homebuyers increasingly ask questions such as:

These considerations increasingly influence purchasing decisions.

Economists have begun describing the possibility of a “climate discount” or “climate bubble.”

Properties with elevated climate risks may experience slower appreciation—or outright depreciation—as markets increasingly recognize long-term exposure.

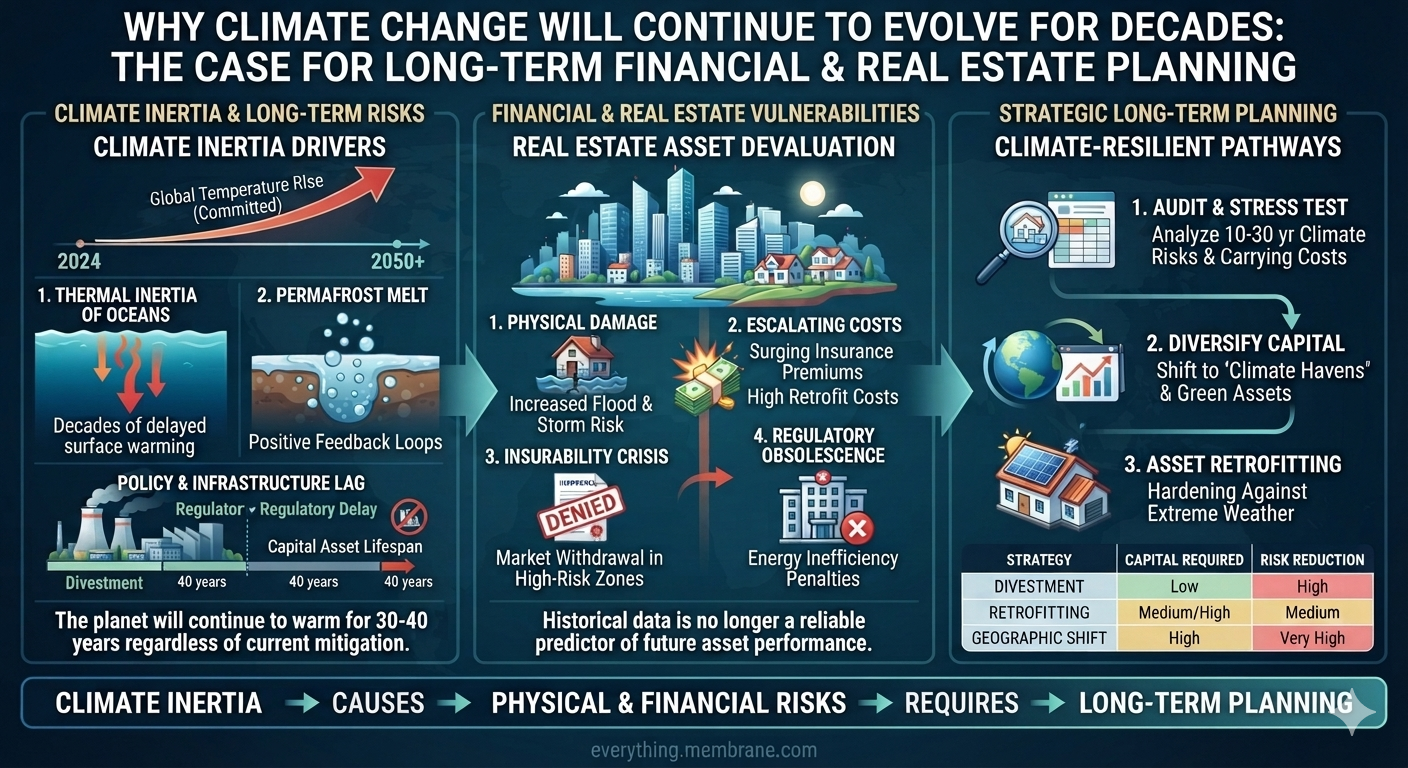

Unlike traditional real estate cycles, climate-related devaluation may persist because the underlying physical risks continue to evolve.

Climate change is transforming real estate from an asset class valued primarily by location into one increasingly valued by resilience.

Future property performance will depend not only on neighborhood desirability but also on:

Investors, lenders, insurers, and homebuyers are already incorporating these factors into financial decisions.

Climate change does not mean that all real estate will suddenly lose value or become uninhabitable. Real estate will remain one of the world’s largest and most important asset classes. However, the factors that determine value are changing.

The greatest risk is not a sudden collapse of the housing market but a gradual repricing of climate risk. Some properties may remain highly desirable for decades, while others may face increasing costs from insurance, maintenance, financing, and regulatory compliance.

Understanding these risks allows homeowners, investors, developers, lenders, and policymakers to make informed decisions. Investments in resilient construction, improved infrastructure, energy efficiency, and thoughtful land-use planning can reduce long-term vulnerability and help preserve property values.

The future of real estate will increasingly be determined not simply by location, location, location, but by location, resilience, and adaptability.

Bottom line: The question is no longer how warm the planet becomes, but how life on Earth can endure when change outpaces our ability to adapt.

We cannot control the laws of physics, but we can control our pollution. The most effective action is to stop burning fossil fuels.