by Daniel Brouse

July 2026

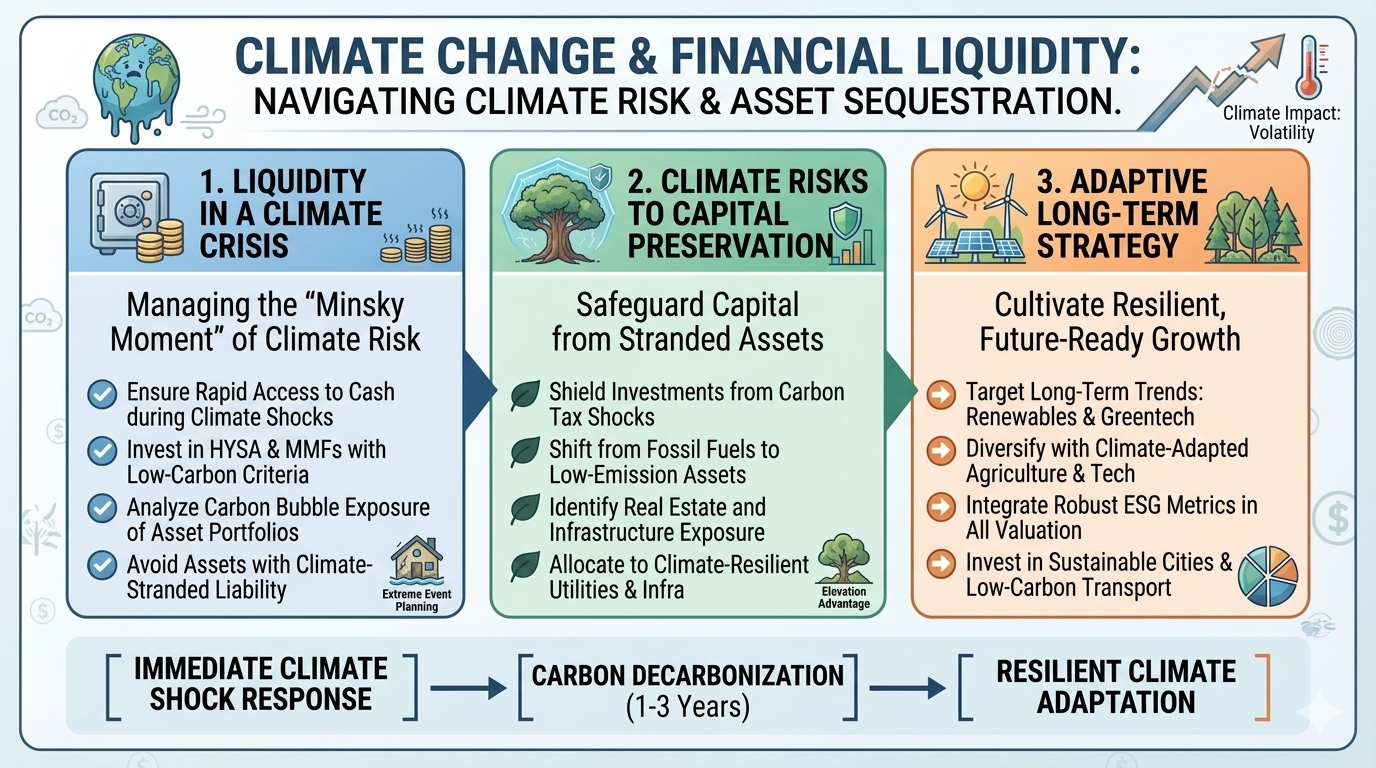

A “Minsky Moment” refers to a sudden, major collapse of asset prices following a long period of market growth and speculative risk-taking. Named after American economist Hyman Minsky and coined by Paul McCulley of PIMCO in 1998, the concept explains why long periods of economic stability inherently build the foundation for severe financial crises.

Climate change is no longer just an environmental issue—it is becoming a financial planning issue. Rising insurance costs, increasing weather-related losses, higher inflation risks, and growing economic uncertainty make protecting capital more important than ever.

The first objective of any sound financial plan is not maximizing returns. It is ensuring that your savings remain available, secure, and able to preserve purchasing power. Liquidity gives you flexibility when unexpected expenses arise, while capital preservation prevents temporary market disruptions from becoming permanent financial losses.

One of the simplest and most effective strategies is to combine a high-yield savings account with a TreasuryDirect account that invests in short-term U.S. Treasury Bills.

Every financial plan should begin with readily accessible cash.

Financial advisors generally recommend maintaining three to six months of living expenses in highly liquid accounts that can be accessed immediately during emergencies.

Good options include:

Unlike long-term investments, these accounts allow you to pay for unexpected expenses without selling stocks or bonds during a market decline.

A high-yield savings account serves as the foundation of your liquidity strategy.

Once you’ve accumulated several hundred dollars beyond your emergency cash reserve, consider opening a TreasuryDirect account with the U.S. Treasury.

TreasuryDirect allows individuals to purchase Treasury securities directly from the federal government without brokerage fees.

Among the available securities, 4-week Treasury Bills (T-Bills) are particularly attractive for capital preservation.

Treasury Bills are considered one of the safest investments in the world because they are backed by the full faith and credit of the United States government.

Additional advantages include:

Because they mature every four weeks, they provide exceptional flexibility if economic conditions change.

Treasury Bills are sold through regularly scheduled government auctions.

Unlike traditional savings accounts, T-Bills are purchased at a discount to their face value.

For example:

The $0.40 difference represents your interest earnings.

When the bill matures four weeks later, the Treasury pays the full face value directly into your account.

Funds used to purchase the bill are automatically withdrawn from your linked bank account after the auction.

Many investors assume all Treasury securities carry identical risk.

They do not.

There is a critical distinction between:

Longer-term bonds are highly sensitive to interest rate changes.

If inflation increases or interest rates rise, existing bonds decline in market value. Investors who need to sell before maturity can lose a substantial portion of their principal.

Short-term Treasury Bills largely avoid this problem.

Because they mature every month, your principal is quickly returned, allowing you to reinvest at current interest rates.

In today’s uncertain economic environment, short-term T-Bills generally provide much greater flexibility and significantly lower interest-rate risk than longer-term government bonds.

TreasuryDirect allows investors to automatically reinvest maturing Treasury Bills.

For example:

This creates a largely automated income stream while maintaining monthly access to your capital.

As interest accumulates in your savings account, it can eventually be invested into additional Treasury Bills, creating a gradual compounding effect.

Another useful Treasury investment is the Series I Savings Bond (I Bond).

Unlike Treasury Bills, I Bonds are specifically designed to protect purchasing power during periods of inflation.

Their interest rate consists of:

When inflation rises, I Bond yields increase accordingly.

During the inflation surge of 2022, newly issued I Bonds briefly paid annualized rates above 9%, illustrating how they can provide meaningful protection during periods of rapidly rising prices.

Additional advantages include:

Because I Bonds cannot be redeemed during their first year and incur a modest interest penalty if redeemed before five years, they are best viewed as a medium-term inflation hedge rather than an emergency fund.

Capital preservation becomes even more important inside retirement accounts.

Money that cannot easily be replaced should generally avoid unnecessary risk.

If you are nearing retirement—or simply wish to reduce volatility—consider investments that prioritize preservation of principal while earning yields comparable to short-term Treasury Bills or other low-risk cash equivalents.

The objective is not to chase maximum returns but to ensure retirement savings remain available when needed.

A resilient financial plan consists of three distinct layers.

| Time Horizon | Objective | Typical Investments |

|---|---|---|

| 0–6 Months | Immediate liquidity | High-yield savings accounts, money market funds |

| 1–3 Years | Capital preservation | 4-week Treasury Bills, I Bonds, short-term Treasury funds, short-term CDs |

| 10+ Years | Long-term growth | Diversified stock index funds, international equities, retirement accounts |

This layered approach allows each dollar to serve a specific purpose rather than forcing every investment to accomplish every objective. While there is no one-size-fits-all allocation, your age, financial obligations, income stability, and future plans should guide how much you keep in each layer.

For individuals following a prudent capital preservation strategy, a sample allocation might look like this:

These allocations prioritize financial flexibility and preservation of principal in an era of increasing economic uncertainty. Younger investors generally have more time to recover from financial setbacks and can afford somewhat greater exposure to long-term growth assets, while those approaching or entering retirement often benefit from emphasizing liquidity and protecting accumulated wealth. Individual circumstances vary, however, so these percentages should be viewed as a prudent framework rather than a universal rule.

Traditional investment principles remain important, but today’s financial environment requires a broader understanding of risk. Investors should consider not only market performance but also their ability to access capital, protect assets, and adapt to changing economic conditions.

Key principles include:

Markets will inevitably fluctuate, but disciplined long-term investing, combined with sound risk management and financial flexibility, has historically rewarded patient investors. The goal is not simply to maximize returns—it is to build a resilient financial foundation capable of adapting to changing economic, environmental, and personal circumstances.

Climate change introduces new financial risks that previous generations rarely considered.

Increasingly, homeowners and investors must account for:

These risks do not necessarily mean financial collapse is imminent. However, they do reinforce the importance of maintaining adequate liquidity and protecting principal. Investors with readily available cash are better positioned to handle emergencies, adapt to changing market conditions, and take advantage of opportunities that arise during periods of economic stress.

Successful investing begins with preserving financial flexibility.

A high-yield savings account provides immediate liquidity. Short-term Treasury Bills offer one of the safest ways to earn competitive returns while protecting principal. I Bonds provide an additional layer of inflation protection for longer-term savings.

Together, these tools create a strong foundation for financial resilience in an increasingly uncertain world.

No investment strategy can eliminate risk entirely, but maintaining liquidity, preserving capital, and investing for long-term growth can help individuals and families navigate economic volatility—including the growing financial challenges associated with climate change—with greater confidence and stability.

Bottom line: The question is no longer how warm the planet becomes, but how life on Earth can endure when change outpaces our ability to adapt.

We cannot control the laws of physics, but we can control our pollution. The most effective action is to stop burning fossil fuels.