by Daniel Brouse

July 2026

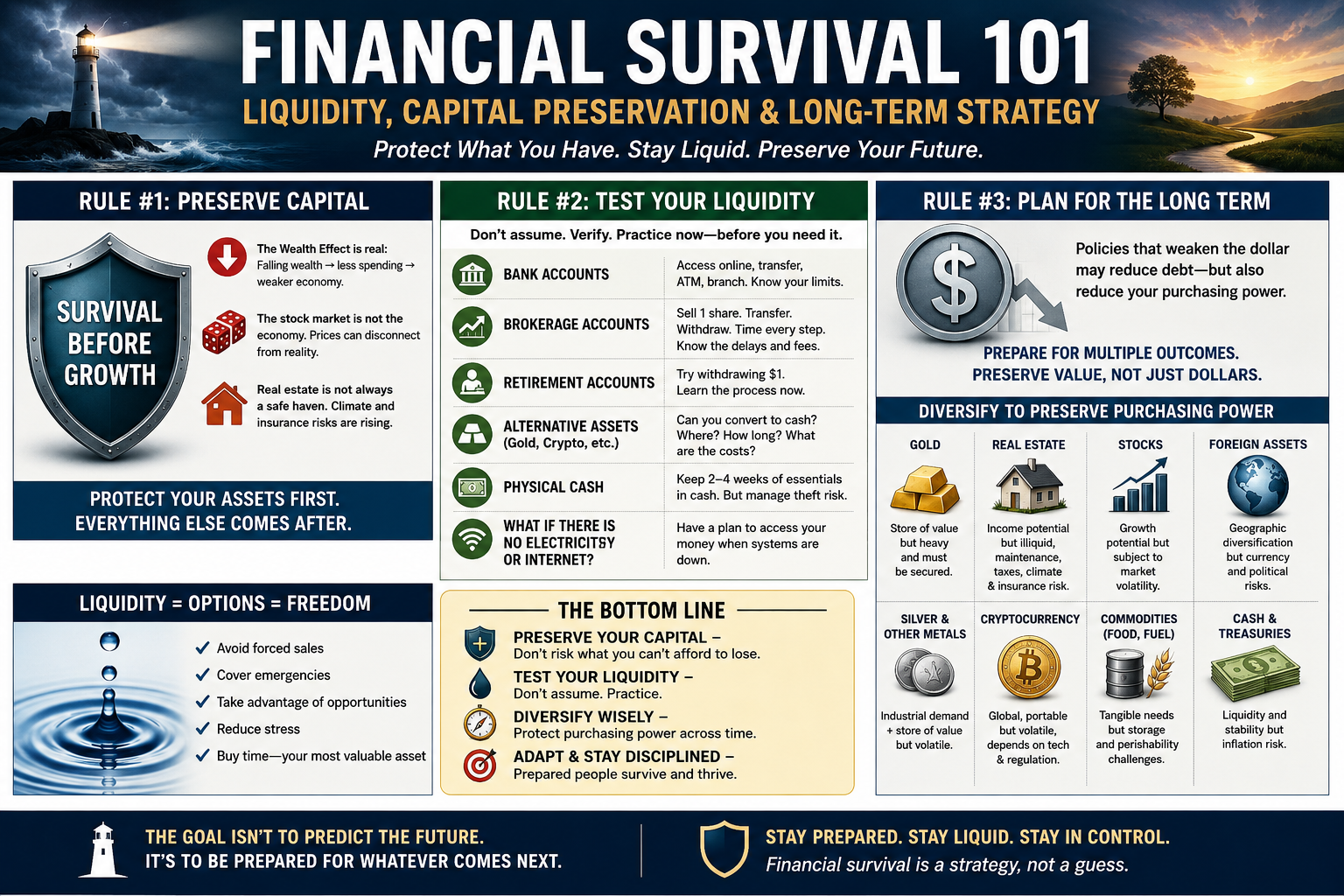

Capital preservation has always been a cornerstone of sound financial planning. In periods of heightened economic uncertainty, however, it becomes the overriding priority.

The goal is not to maximize returns at all costs. It is to ensure that you retain enough purchasing power and financial flexibility to navigate whatever comes next.

One concept increasingly influencing both Wall Street and Main Street is the Wealth Effect.

When household wealth rises—through higher stock prices, appreciating home values, or growing retirement accounts—people generally feel more confident. They spend more, borrow more, and invest more.

The opposite is equally true.

When people perceive themselves to be poorer, they begin cutting expenses. Vacations are postponed. New cars aren’t purchased. Home renovations are delayed. Restaurants see fewer customers. Businesses experience lower sales, which often leads to reduced hiring and layoffs.

The decline becomes self-reinforcing.

What begins as falling asset prices can eventually slow the broader economy.

One of the biggest mistakes investors make is assuming that the stock market and the economy move together.

Over long periods they are related.

Over shorter periods they often are not.

Modern financial markets are increasingly driven by institutional trading, derivatives, leverage, algorithmic trading, and investor sentiment. Prices can become disconnected from underlying economic fundamentals for extended periods.

That means:

Markets frequently overshoot in both directions.

Investors should avoid making emotional decisions based solely on market movements.

For generations, real estate has been viewed as one of the safest long-term investments.

That assumption deserves closer examination.

Unlike stocks or bank deposits, real estate is highly illiquid. Selling a property can take weeks or months, and transactions involve significant costs, including commissions, taxes, legal fees, inspections, and financing contingencies.

Climate-related risks are adding another layer of uncertainty.

In many regions, insurance premiums have risen dramatically or insurers have withdrawn from markets altogether. Mortgage lenders are increasingly evaluating climate exposure, flood risk, wildfire danger, and long-term property resilience.

Some coastal communities, wildfire-prone regions, and flood zones are already experiencing declining property values, slower sales, or reduced insurance availability.

Examples include portions of:

These trends do not mean that all real estate is at immediate risk. Many properties may remain attractive for decades. However, location-specific climate and insurance risks are becoming increasingly important considerations in short- and medium-term financial planning. Over the longer term, climate change is expected to affect virtually all real estate to varying degrees. The nature and severity of those risks will differ by location, but no property is likely to remain entirely insulated from changing climate conditions, rising insurance costs, evolving regulations, or shifting market preferences.

Real estate should no longer be evaluated solely by neighborhood, schools, and appreciation potential. Future insurability, financing availability, infrastructure resilience, and climate exposure are becoming equally important.

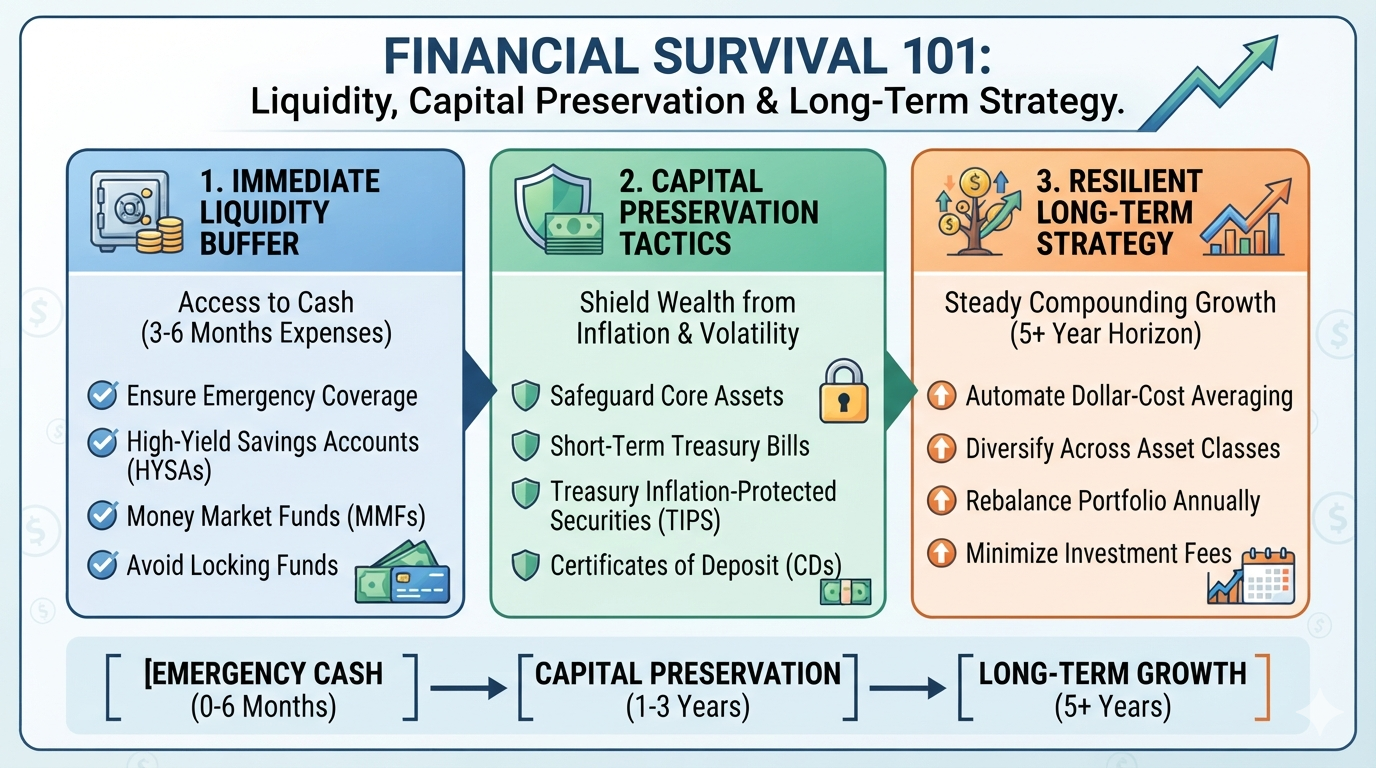

After protecting capital comes a second priority:

Liquidity.

Liquidity measures how quickly an asset can be converted into usable cash without suffering significant losses.

During normal times, liquidity is often taken for granted.

During financial stress, it becomes priceless.

Many investors discover too late that assets they believed were readily available actually require days, weeks, or months to access.

That is why liquidity should be tested—not assumed.

Think of this as a financial fire drill.

You hope you’ll never need it.

But you’ll be grateful you’ve practiced.

Can you:

Know your daily withdrawal limits.

Understand your bank’s policies before an emergency occurs.

Try the complete process:

Time every step.

Record:

A brokerage balance isn’t liquid until the money reaches your wallet.

Many retirement accounts allow withdrawals under certain circumstances.

Even if taxes or penalties apply, learn the mechanics now.

Understanding the paperwork, timing, and restrictions before an emergency reduces stress later.

If you own gold or silver, ask yourself:

Owning precious metals is different from converting them into cash.

Practice the process.

Crypto markets operate around the clock, but converting digital assets into spendable cash involves several steps.

Can you:

Test a small transaction.

Don’t wait until markets become volatile.

Most financial planners recommend maintaining an emergency reserve.

Consider keeping enough physical cash to cover several weeks of essential expenses while avoiding excessive amounts that create theft or security risks.

Cash remains useful during temporary disruptions to banking networks, power outages, or payment systems.

Bottom line: The question is no longer how warm the planet becomes, but how life on Earth can endure when change outpaces our ability to adapt.

We cannot control the laws of physics, but we can control our pollution. The most effective action is to stop burning fossil fuels.